U.S. Dollar & Mortgage Rates

Introduction

"The only way out is through." - Robert Frost

March is quickly becoming one of my least favorite months. In the past few years, March has brought us the COVID breakout in 2020, the regional bank crisis in 2023, and currently, the war with Iran. Just missing the cut was the Tariff Tantrum on April 2nd last year.

Beyond the obvious price of oil, there are two specific things I'm monitoring for signs of improvement.

Interest Rates

One of the knock-on effects of this situation is the increase in interest rates.

When discussing interest rates, it is important to clarify which one is being discussed, as they can mean different things.

The rate on a two-year government bond jumped from around 3.4% before the conflict began to 4% just a few days ago.

This is important because the two-year rate is seen as a predictor of the Federal Reserve's future interest rate policy.

A jump of this magnitude means the bond market switched from expecting future rate cuts to potential rate hikes.

The other object of my attention is the rate on a ten-year government bond.

Probably the most widely tracked interest rate in the world, it has major implications for everything from mortgage rates (more on that later) to the stock market.

Rule of thumb: we don’t want to see it move too quickly in either direction.

If it is rising too fast, it suggests the market is likely bracing for an inflationary environment.

If it is falling too fast, it could mean a recession is on the horizon.

Right now? It’s climbing uncomfortably fast (for me, at least), but has yet to reach escape velocity.

The U.S. Dollar

Remember last month’s issue when I discussed the dawning of a new cycle of dollar weakness?

No? Ok, good, because a lot has changed in the last month.

After a highly publicized demise, the Dollar tapped into its inner Mark Twain and said, “Those reports have been greatly exaggerated.”

We learned the Dollar is *still* viewed as a safe haven during times of crisis.

Don’t take my word for it—take the market’s.

Relative to other major currencies, the Dollar recently reached its highest level in almost a year.

Similar to interest rates, I would prefer a subdued Dollar—no sudden movements, please.

Conclusion

There is a lot at stake in the Middle East right now, way beyond financial markets.

For many reasons, we hope for a swift end to this conflict.

Chart Of The Month

What Caught Our Eye

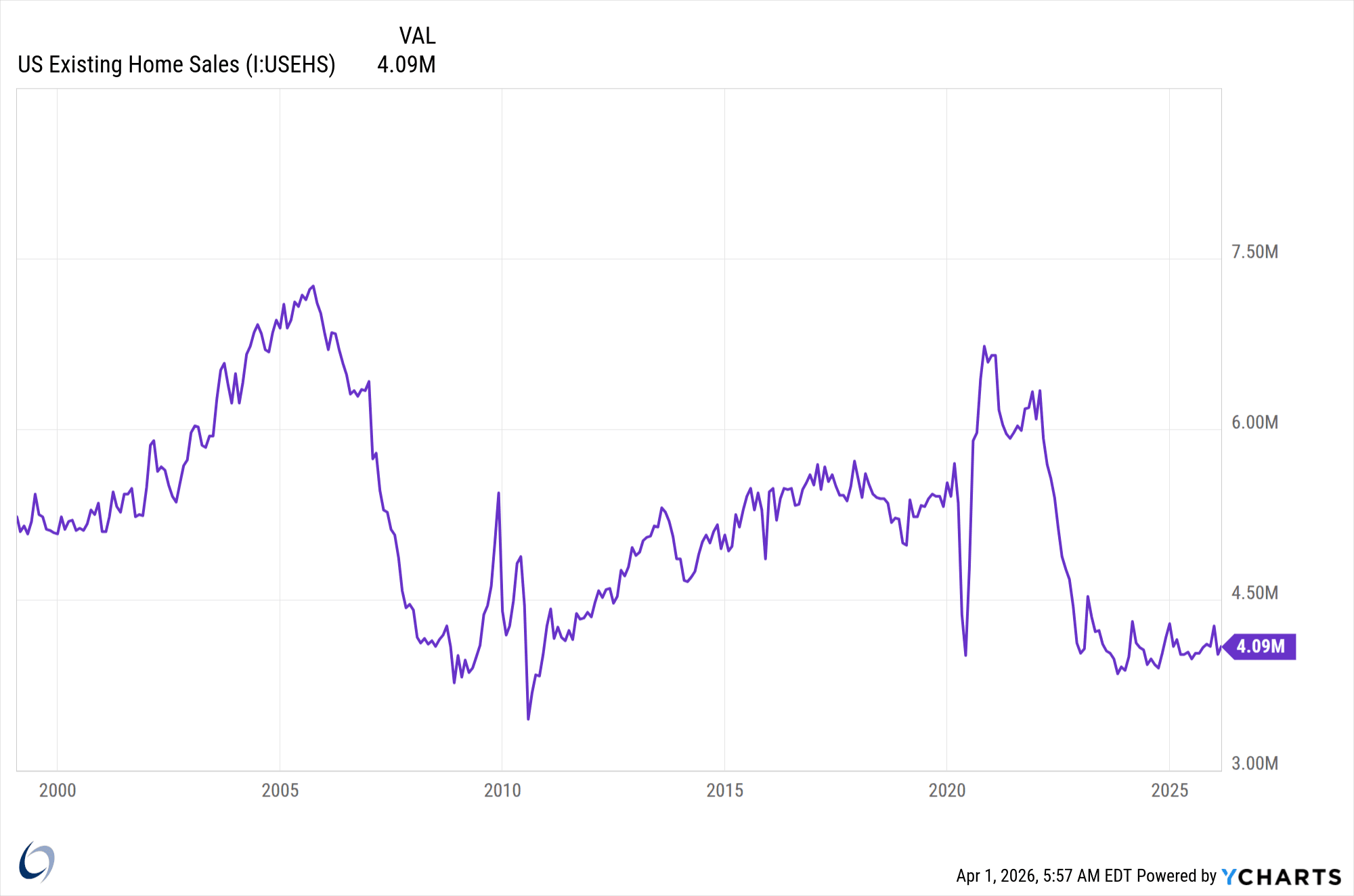

“With mortgage rates where they are, we feel stuck.”

That was from a conversation I had with a friend on Saturday, but honestly, it’s a common refrain among Americans these days.

I mentioned in the last section how important the interest rate on a 10-year government bond is because of its impact on mortgage rates.

The chart above shows why.

Sales of existing homes have hovered around post-housing bubble levels in absolute terms for the past two years.

Relative to the overall housing supply, we are at an all-time low.

High mortgage rates have a two-pronged effect—they make home purchases more expensive for renters, and they keep current homeowners “trapped” with a 3-4% mortgage.

Housing’s impact on the economy is multifaceted.

Rents are consuming the highest percentage of disposable income in history.

The National Association of Realtors estimates $90k of transaction-linked spending for each home sale.

Job-related mobility is constrained, keeping home-owning workers in their current locations rather than allowing them to take higher-paying, better jobs elsewhere.

Property taxes are suppressed, impacting local governments.

For all the reasons listed above, a lower interest rate on the 10-year government bond would be a welcome sign for the housing market.

Continuum Multimedia

Podcast

Be sure to subscribe on your podcast player of choice!

YouTube

Pat and I discussed the impact of the war on financial markets.